Global Oil Supplies as Reported

My post is mainly an update to

Global Oil Supplies as Reported by EIA's International Petroleum Monthly for September 2010,

based on data which the EIA reported in the past few days. I will also

briefly present updated information regarding OECD and Non OECD oil

supplies/consumption.

The stacked columns show crude oil and condensates supplies split

among OPEC, Russia and ROW (Rest Of World which also includes OECD),

from January 2001 through August 2010. The development in the average

monthly oil price is plotted on the left hand y-axis.

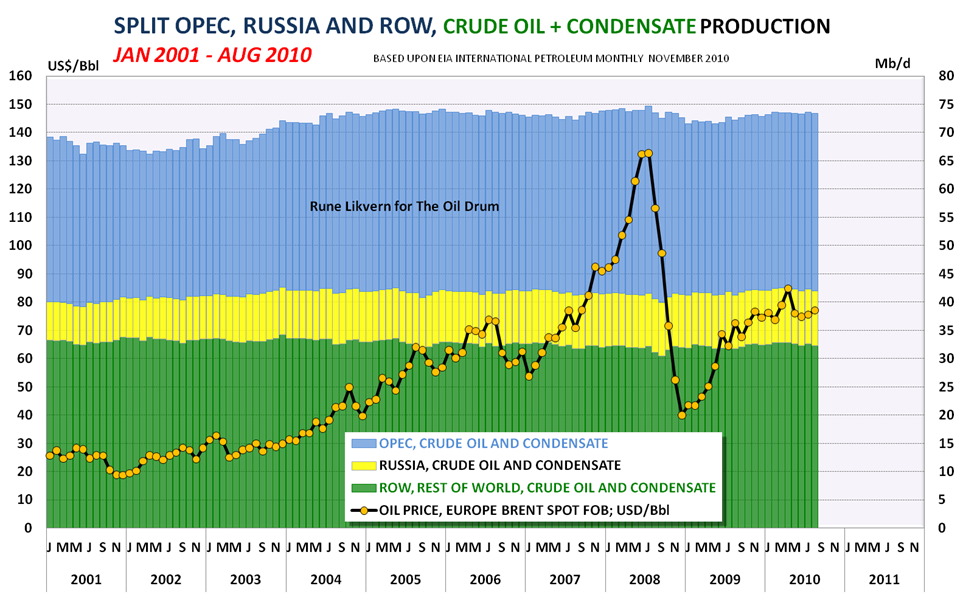

The stacked columns show crude oil and condensates supplies split

among OPEC, Russia and ROW (Rest Of World which also includes OECD),

from January 2001 through August 2010. The development in the average

monthly oil price is plotted on the left hand y-axis.

Note that world oil production has been on a plateau, from late 2004

to the present, with a small dip when prices dropped in late 2008 to

early 2009. This graph considers crude and condensate only, excluding

natural gas liquids and other forms of liquid energy, such as biofuels.

DISCLAIMER: The author holds no positions in the oil/energy market that may be affected by the content of this post.

NOTE: Scaling varies from chart to chart and some charts are not zero

scaled. Labels indicate whether graphs are on an "all liquids" or

"crude and condensate" basis.

Figure 01: The stacked columns in the diagram above show

development in global supplies of crude oil and condensate, NGL and

other liquid energy from January 2001 through August 2010. The

development in the average monthly oil price is plotted on the left hand

y-axis. NOTE: Diagrams based upon EIA data may be subject to future

revisions.

Figure 02: The stacked columns shows crude oil and

condensates supplies split among OPEC, Russia and ROW (Rest Of World;

which also includes OECD), from January 2001 and as of August 2010. The

development in the average monthly oil price is plotted on the left hand

y-axis.

Figure 01: The stacked columns in the diagram above show

development in global supplies of crude oil and condensate, NGL and

other liquid energy from January 2001 through August 2010. The

development in the average monthly oil price is plotted on the left hand

y-axis. NOTE: Diagrams based upon EIA data may be subject to future

revisions.

Figure 02: The stacked columns shows crude oil and

condensates supplies split among OPEC, Russia and ROW (Rest Of World;

which also includes OECD), from January 2001 and as of August 2010. The

development in the average monthly oil price is plotted on the left hand

y-axis.

Over the period covered by the graph (2001 to present), growth in Non

OPEC supplies have primarily come from Russia. Oil supplies from the

"Rest of World" (ROW) have not grown.

The long bumpy plateau from late 2004 to the present illustrates that

huge swings in oil prices in recent years have had only a small impact

on crude oil and condensate supplies.

EIA in their STEO (Short Term Energy Outlook) for November 2010

projected a slight decline in OECD and Russian petroleum supplies from

2010 to 2011, but a smaller decline than in the September STEO had

shown. Under most circumstances, it could be expected that most of these

declines would be offset by growth in OPEC supplies.

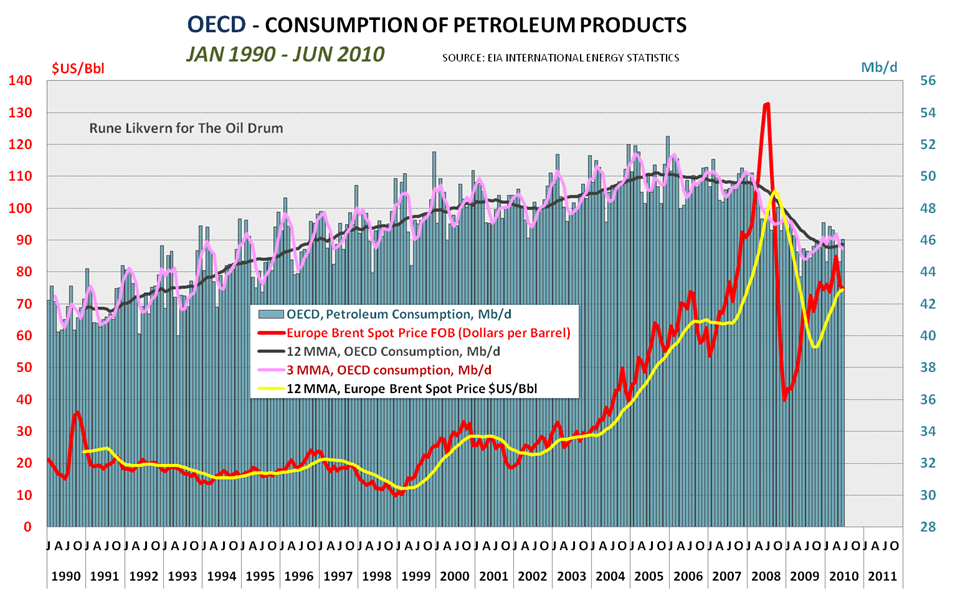

Figure 03: The diagram above shows development in OECD

consumption of petroleum products between January 1990 and June 2010

together with the development in the oil price.

Figure 03: The diagram above shows development in OECD

consumption of petroleum products between January 1990 and June 2010

together with the development in the oil price.

In the recent months, petroleum consumption within OECD has seen some

growth and this coincides with the recent growth in the oil price.

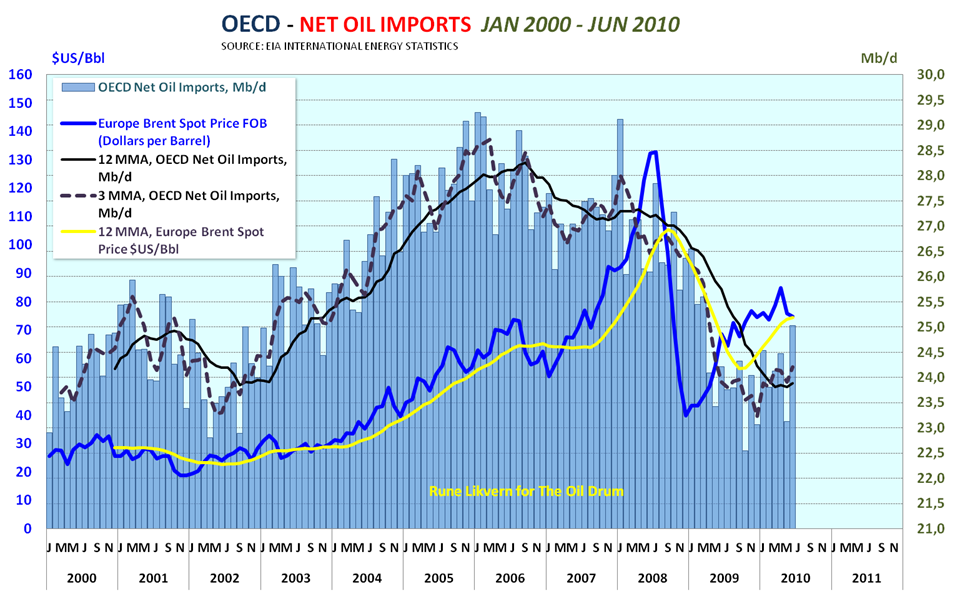

Figure 04: The diagram shows development in net oil imports for OECD from January 2000 through June 2010.

Figure 04: The diagram shows development in net oil imports for OECD from January 2000 through June 2010.

This diagram shows that the recent oil price growth happened as OECD

again started increasing oil imports. This is one of the indicators

suggesting that the oil price now has strong support based on

fundamentals.

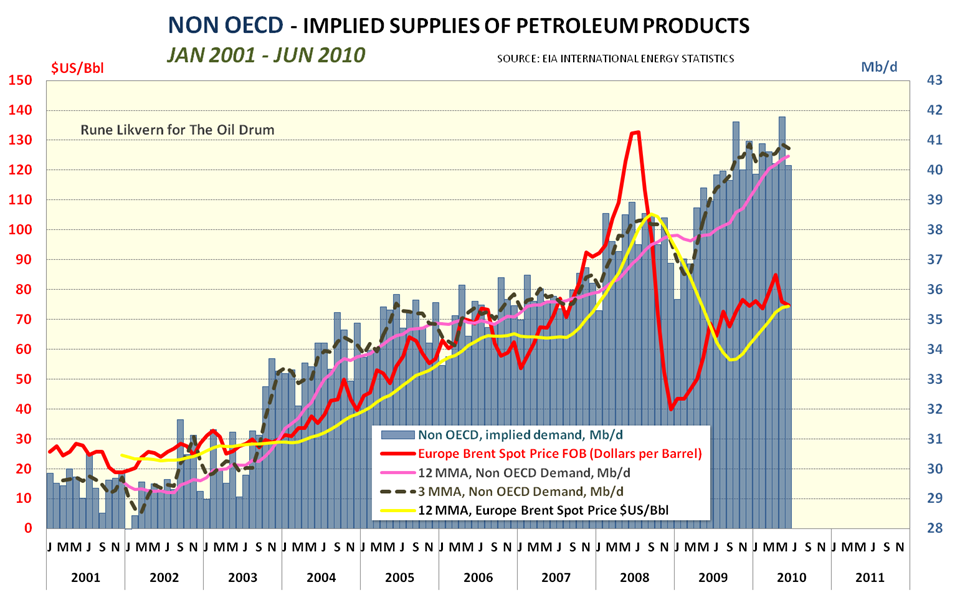

Figure 05: The above diagram shows implied demand for liquid

energy from Non OECD countries from January 2001 through June 2010. (I

describe it as implied demand as the diagram shows the difference

between total global supplies of liquid energy and OECD supplies

(production + net imports)).

Figure 05: The above diagram shows implied demand for liquid

energy from Non OECD countries from January 2001 through June 2010. (I

describe it as implied demand as the diagram shows the difference

between total global supplies of liquid energy and OECD supplies

(production + net imports)).

Recently, demand for petroleum products from Non OECD seems to have

leveled out as illustrated by the 3 MMA (3 Month Moving Average). (I use

the 3MMA both to more easily identify seasonal variations and also to

act as a “pilot” for trends over several months.)

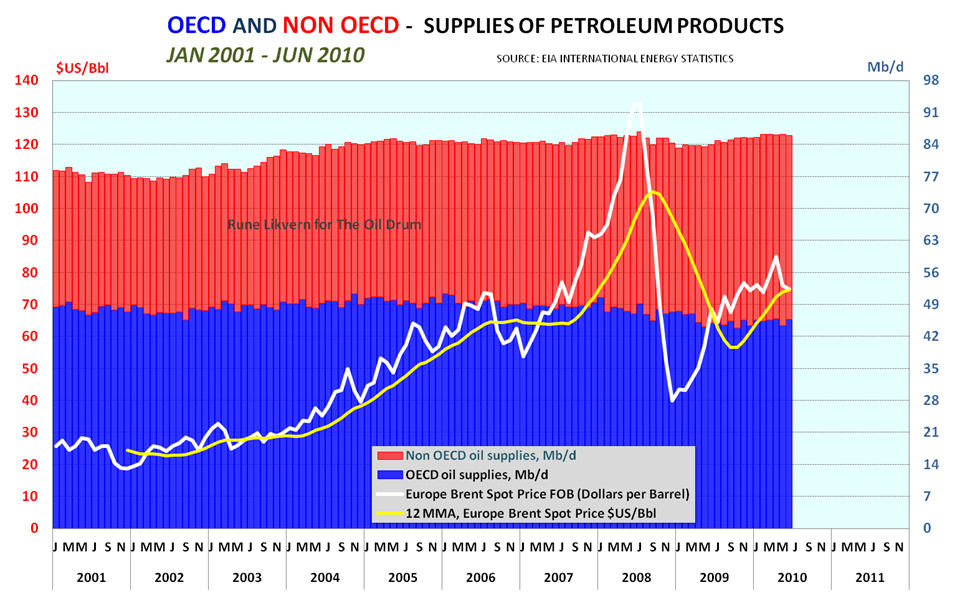

Figure 06: The stacked columns show the split between OECD

and Non OECD supplies of liquid energy from January 2001 through June

2010. The average monthly oil price is also plotted on the left hand

y-axis.

Figure 06: The stacked columns show the split between OECD

and Non OECD supplies of liquid energy from January 2001 through June

2010. The average monthly oil price is also plotted on the left hand

y-axis.

If we start with Figure 05 there clearly was a strong growth in

demand from Non OECD starting early in 2009. From the diagram it shows

the price grew with the demand growth from Non OECD. OECD demand was

tanking at the time. To me this is a strong indicator that price in this

period was driven by Non OECD demand.

As OECD production continues to decline, a growing need for imports

into OECD (ref figure 04 in this post) is expected to add upward

pressure to the oil price. Oil imports into OECD will normally tend to

be higher during the heating season (winter in the Northern Hemisphere)

and this suggests an upward pressure on the oil price in the months

ahead.

Within a couple of weeks, I hope to post here on TOD an in-depth

analysis that shows that at the current costs (as of first half of

2010), one can expect that in the U. S., an average annual oil price of

$80 - 85/Bbl (Brent spot) results in GDP exclusive of energy

expenditures that does not grow. This means that the present growth in

U.S. GDP covers growing energy expenditures. Energy expenditures are

costs for petroleum products, plus energy resources for non energy use

(asphalt, coke, petrochemical feedstock etc.), natural gas and

electricity).

Figure 07: The stacked columns show each OPEC member’s crude

oil supplies and OPEC’s supplies of lease condensates and NGLs from

January 2001 through August 2010. The average monthly oil price is also

plotted on the left hand y-axis.

Figure 07: The stacked columns show each OPEC member’s crude

oil supplies and OPEC’s supplies of lease condensates and NGLs from

January 2001 through August 2010. The average monthly oil price is also

plotted on the left hand y-axis.

The recent data from EIA shows a small growth in supplies of crude

oil, condensates and NGLs from OPEC. (Lease condensates and NGLs are

presently not part of OPEC's quota arrangements.)

To me, the recent growth in the oil price (adjusted for fluctuations

in the value of the US Dollar) is a signal calling upon increased crude

oil deliveries from OPEC.

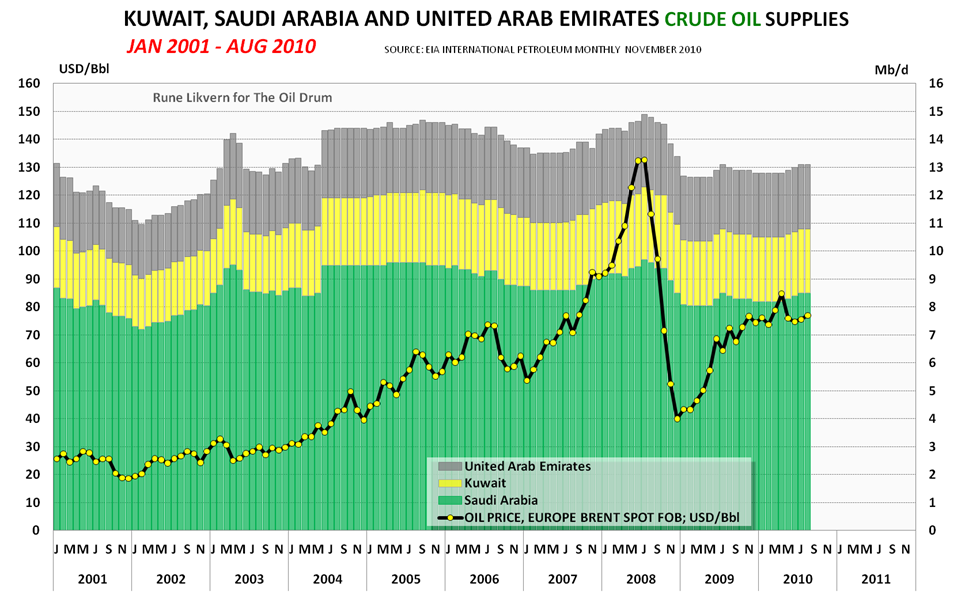

Figure 08: The diagram above shows crude oil supplies from

January 2001 through August 2010 for Kuwait, Saudi Arabia and United

Arab Emirates.

Figure 08: The diagram above shows crude oil supplies from

January 2001 through August 2010 for Kuwait, Saudi Arabia and United

Arab Emirates.

I believe most of present global spare

marketable crude oil

capacity is to be found amongst the 3 exporters presented above. Saudi

Arabia increased their crude oil supplies by 300 kb/d between April and

July of this year. It is not clear whether one can conclude that this

caused some retreat in the oil price, but it is an interesting

coincidence.

Figure 09: The stacked columns shows development in crude oil

supplies from the 9 other OPEC members. The average monthly oil price

is plotted on the left hand y-axis.

Figure 09: The stacked columns shows development in crude oil

supplies from the 9 other OPEC members. The average monthly oil price

is plotted on the left hand y-axis.

Total crude oil supply from the 9 OPEC members above have remained

relatively high and flat during the recent months, suggesting that these

countries are pumping at maximum levels, regardless of price.

In summary, November's International Petroleum Monthly supports a continuation of the trends I had noted in my

earlier post.

In other words, world economies are still growing, putting more

pressures on oil prices. By the end of 2011, my earlier analysis showed

that the OPEC spare supply margin may be depleted. The next few months

may be interesting ones!

SOURCES:

[1] EIA, INTERNATIONAL PETROLEUM MONTHLY, NOVEMBER 2010

[2] EIA, INTERNATIONAL ENERGY STATISTICS

[3] EIA, SHORT TERM ENERGY OUTLOOK, NOVEMBER 2010

Currently, the amount of electricity produced is restricted according to the production capability of the power grid. During peak usage times, the grid is taxed to the max, making it more vulnerable to failure. This supply versus demand system supports the high energy costs that we as consumers are faced with. What if

Currently, the amount of electricity produced is restricted according to the production capability of the power grid. During peak usage times, the grid is taxed to the max, making it more vulnerable to failure. This supply versus demand system supports the high energy costs that we as consumers are faced with. What if